FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022

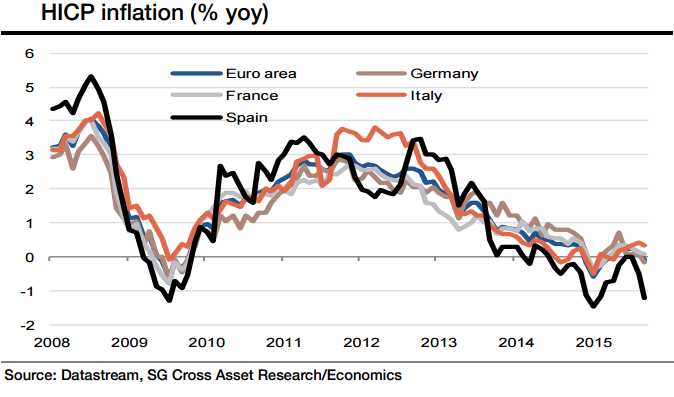

While food prices continue to contribute positively to headline inflation, and core inflation remains stable, oil prices have remained low at around $45-50 per barrel, ensuring that the energy contribution to inflation remains negative. After slowing to 0.8% in 2014 from an average of 1.1% in 2013, core inflation upped the tempo somewhat in 2015, increasing from 0.6% in January to 0.9% in September.

"We maintain that the pace of core inflation is likely to be sluggish and will average 0.8% in 2015 before gradually increasing to 1.2% in 2016", says Societe Generale.

Euro area inflation in September fell into negative territory for the first time since March 2015. In yoy terms, it fell into the red (-0.1%), with the energy component at -8.9% yoy. Prices in Italy slowed to 0.2%, Germany fell into negative territory (-0.2%), while Spain, where inflation was already negative, saw a further significant fall to -1.2%.

"Given the base effects from the sharp decline in oil prices towards the end of 2014, our Brent forecasts of around $50 per barrel by year-end and the estimated depreciation of EUR/USD to 1.05 towards the end of 2015, we expect headline inflation to increase by year-end", added Societe Generale.

The inflation turnaround towards the end of the year is likely to pick up pace in 2016, underpinned by the expected economic recovery, the pass-through of past declines in the euro exchange rate and the assumption of a recovery in oil prices in the year ahead. These factors, alongside higher food prices, should see core inflation converge with headline inflation.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Fuel prices push Euro area headline inflation into negative territory

Wednesday, September 30, 2015 8:23 PM UTC

Editor's Picks

- Market Data

Most Popular