Open-Source AI Models Gain Ground as Enterprises Seek Lower-Cost Alternatives, Citi Says

Open-Source AI Models Gain Ground as Enterprises Seek Lower-Cost Alternatives, Citi Says  Economic pessimism has set in – but there are reasons for Australians to be hopeful

Economic pessimism has set in – but there are reasons for Australians to be hopeful  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum

Gold Surges Above Key EMAs, Bulls Eye Resistance Amidst Bullish Momentum  Should I take zinc or eat oysters to ward off colds, boost my immune system or improve fertility?

Should I take zinc or eat oysters to ward off colds, boost my immune system or improve fertility?  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?  Europe Heatwave Creates Growth Opportunity for Carrier, Trane, and Johnson Controls, Citi Says

Europe Heatwave Creates Growth Opportunity for Carrier, Trane, and Johnson Controls, Citi Says  Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

Morgan Stanley Sees Chinese Auto Market Recovery Gaining Momentum in Late Summer

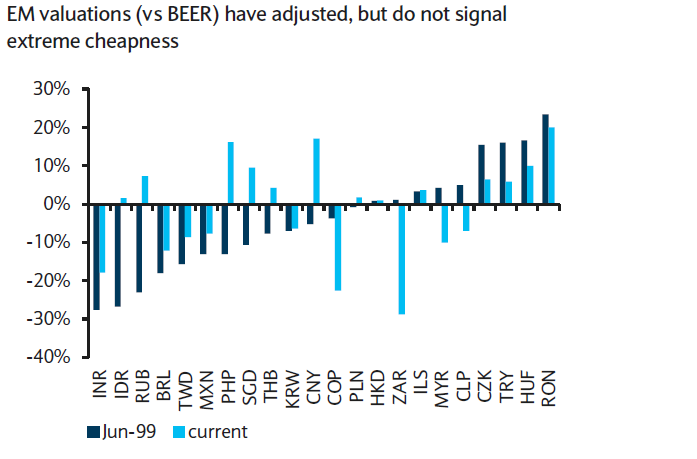

Although some currencies have weakened sharply due to global slowdown especially China, all EM FX do not appear to have overshot. EM Asia FX will face the brunt of slowing Chinese growth and a weaker CNY. Korea and Taiwan are particularly vulnerable given their general openness to trade and their trade exposure to China.

In addition, Korea is actively looking to recycle its current account surplus while having less room to boost economic conditions via policy easing. In Taiwan, exports have been weak recently and could face further pressure from slowing growth in China.

While Elsewhere in EM corporate, we think Hong Kong issuers are likely to benefit from the outflows triggered by a change in China's FX policy. Liquidity and deposits in Hong Kong banks are likely to increase substantially, creating a bid for the bonds they typically buy.

We recommend buying 6 month USDKRW and USDTWD NDFs. We have also initiated a long USDCNH 6m forward recommendation as forwards are not pricing in the extent of weakness in CNY/CNH.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FXWirePro: Korea capitalizing trade surplus despite Chinese slowdown – 6M forwards for hedging

Tuesday, September 29, 2015 1:24 PM UTC

Editor's Picks

- Market Data

Most Popular