FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Wall Street Slides as AI Stocks Tumble Following South Korea Tech Sell-Off

Wall Street Slides as AI Stocks Tumble Following South Korea Tech Sell-Off  US Dollar Hits One-Year High as Hawkish Fed Outlook Overshadows Middle East Developments

US Dollar Hits One-Year High as Hawkish Fed Outlook Overshadows Middle East Developments  Gold Prices Mixed as Stronger Dollar Offsets Safe-Haven Demand Amid U.S.-Iran Peace Talks

Gold Prices Mixed as Stronger Dollar Offsets Safe-Haven Demand Amid U.S.-Iran Peace Talks  Oil Prices Drop as Strait of Hormuz Shipping Recovers

Oil Prices Drop as Strait of Hormuz Shipping Recovers  Japan, U.S. Discuss Yen Weakness as Currency Intervention Concerns Grow

Japan, U.S. Discuss Yen Weakness as Currency Intervention Concerns Grow  Gold Falls Below $4,000 as Strong Dollar and Fed Rate Hike Expectations Weigh on Prices

Gold Falls Below $4,000 as Strong Dollar and Fed Rate Hike Expectations Weigh on Prices  Japan Keeps Markets Guessing as Yen Nears 40-Year Low, Raising Intervention Risks

Japan Keeps Markets Guessing as Yen Nears 40-Year Low, Raising Intervention Risks  100+ Global Companies Push Governments to Prioritize Electrification for Economic Growth

100+ Global Companies Push Governments to Prioritize Electrification for Economic Growth  Oil Prices Slip as Iran Sanctions Relief and Hormuz Shipping Recovery Ease Supply Concerns

Oil Prices Slip as Iran Sanctions Relief and Hormuz Shipping Recovery Ease Supply Concerns  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  US Dollar Climbs to One-Year High as Fed Rate Hike Expectations Surge

US Dollar Climbs to One-Year High as Fed Rate Hike Expectations Surge  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

The euro-zone’s services sector has held up relatively well so far this year. However, we expect spill-overs from the industrial recession and slowing employment growth to take a toll in the coming months. The latest business surveys point to a sharp deceleration in the sector in Q4, according to the latest research report from Capital Economics.

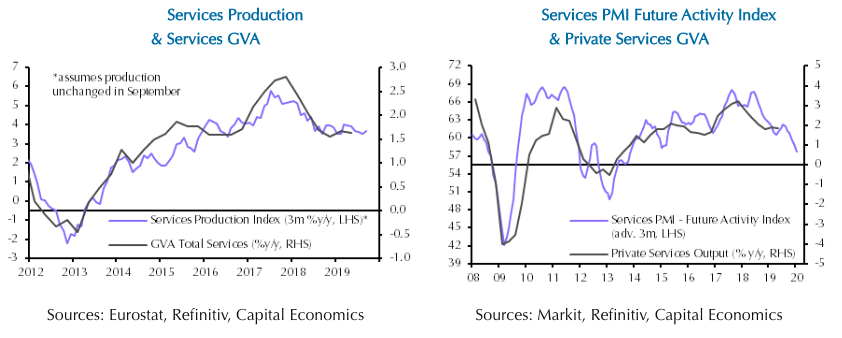

In recent months, many commentators have taken comfort from the fact that, while the euro-zone’s industrial sector is in a deep recession, services are holding up better. Admittedly, it has not been immune to the industrial downturn: services output growth slowed from 2.4 percent in 2017 to 1.6 percent y/y since late 2018, with the weakness concentrated in areas most exposed to manufacturing. But the services sector has not slowed any further over the course of 2019.

The latest data suggest that services have maintained their pace in the third quarter. There is yet no breakdown of third-quarter GDP for the euro-zone as a whole, but monthly production data for services are available up to August.

These are not identical to the national accounts data because they exclude “finance and insurance”, “arts, entertainment and recreation” and “public administration, health and education”. But they are quite closely correlated with the quarterly data.

The year-on-year change in this index points to annual services output growth remaining around 1.6 percent in Q3. This is broadly consistent with the message from the latest national GDP data, which showed services output growth was unchanged in France and slightly slower in Spain, the report added.

Not surprisingly, the sectors most exposed to industry have continued to struggle the most. In August and September, activity in “professional, scientific and technical activities” slowed sharply while “transportation and storage services” growth softened.

But information and communications services, which is less exposed to industry, slowed too, perhaps indicating that the weakness is spreading.

Looking ahead, the latest business surveys point to a steeper downturn to come. The services PMI has dropped from 58.0 in January 2018 to 52.2 in October this year, and the ESI has also declined. In the PMI surveys, firms have cited domestic and global political uncertainty, and spill-overs from manufacturing, as weighing on activity. Slower employment growth is also playing a part.

The euro-zone services PMI’s future activity index, which measures whether businesses expect their output in a year’s time to be higher, the same or lower than currently, is close to a five-year low. On past form, it points to euro-zone private services output growth slowing sharply in the coming months. This is also true for three of the euro-zone’s four largest economies.

"The upshot is that the outlook for the euro-zone’s services sector is weakening. With industry likely to remain in recession next year, we think that annual GDP growth will slow to only around 0.5 percent," Capital Economics further commented in the report.