Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  Indonesia Passes New Central Bank Law, Raising Investor Concerns Over Policy Independence

Indonesia Passes New Central Bank Law, Raising Investor Concerns Over Policy Independence  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

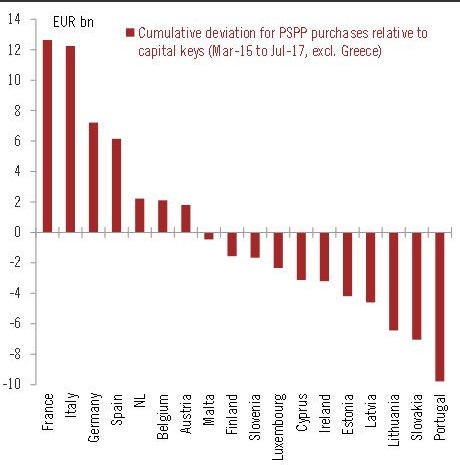

When the European Central Bank (ECB), the latecomer in the Quantitative Easing (QE) program announced its Public Sector Purchase Program (PSPP) in 2015, it was said that the program would follow the central bank’s capital key structure. The structure is based on individual countries or central bank’s contribution to European Central Bank’s (ECB) base capital. However, in reality, after years of PSPP, the deviation from key capital ratio is quite large and the gap is likely to grow if ECB continues further on its bond buying program.

According to data, while ECB bought more bonds than key capital for Italy, France, Germany, Spain, Netherlands, and Belgium, it has bought lesser amounts than the key capital for rest of the Eurozone. ECB didn’t buy any Greek bonds. The gap is highest for Franc and Italy with around €12 billion. And on the downside, the gap is largest for Portugal (approx. €10 billion).

The gap could continue for many economies and even expand if ECB continues to expand its balance sheet without changing the current rules. To give an example, as of now, ECB has bought €10 billion less of Portugal bonds than key capital ratio requires but the current bond purchase has already hit 30 percent issuer limit, whereas the rules bar ECB from buying more than 33 percent bonds for any issuer.