USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings

Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings  Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season

Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook

Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher

Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher

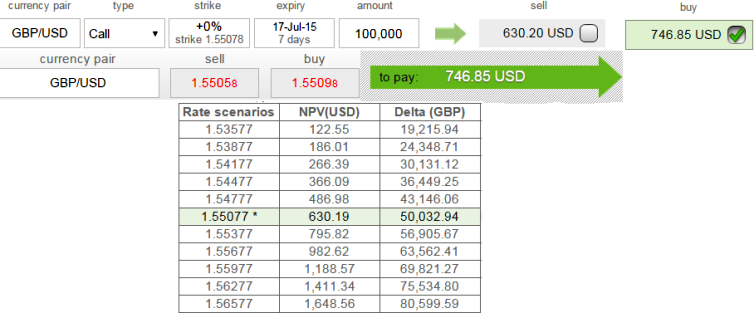

Delta signifies the equivalent FX spot outrights of a given position. This is the sensitivity of a position's value with respect to the spot rate.

This is useful to monitor directional risks so you may know how much your option's value will increase or diminish as the underlying market moves.

A higher delta value is desirable for an option holder, whilst a delta close to zero is desirable for the option writer; a buyer wants their option to become more valuable whilst a seller wants the option to become less valuable.

For an instance, as we can see in the chart that overall position in GBPUSD behaves as if it was long 50,032.94 GBPUSD spot.

But in real terms, if at all GBPUSD spot were to move up by one pip then the relative sensitivity in option premium would be USD 0.5003. To hedge a call, one would invest the option price proceeds into Δt∗St+Bt=ct (where Δ=delta).

These terms may seem quite strange to you but nothing rocket science hidden in it, we would run you through these blackscholes in upcoming articles.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Why delta is crucial in option strategy

Friday, July 10, 2015 1:59 PM UTC

Editor's Picks

- Market Data

Most Popular