Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027

Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027  Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook

Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings

Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone

Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

Since the recent Fed commentary suggests that a September hike is unlikely, whether the Fed hikes later in the year would depend on the evolution of economic data, as well as financial conditions.

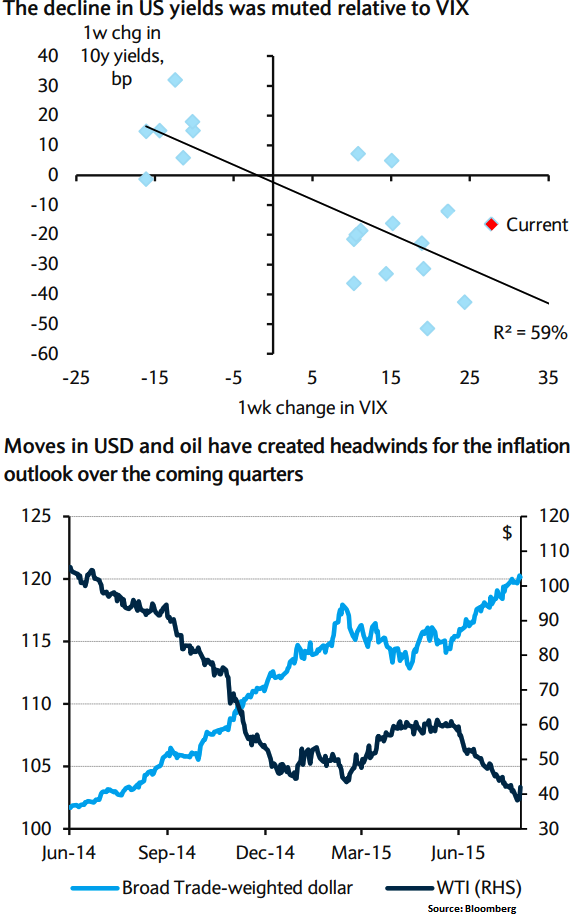

Given the recent increase in implied volatility and the Fed emphasizing a gradual path of policy, we recommend selling 3m5y straddles. The price action in the bond markets was relatively contained in the face of a sharp increase in risk aversion; even as VIX rose as high as 50pts, 10y US yields rallied only 10-15bp and failed to decline materially below 2% except for a brief period of time.

Recent dovish commentary from the Fed and the rally in energy prices have led to a rebound in risk assets from the lows. Even as 10y yields at 2.2% are only back to where they were early last week, the 5s30s Treasury curve has steepened sharply. Although the recent Fed hiking rate seems unlikely for now but whether the Fed hikes later in the year would depend both on the evolution of economic data and financial conditions.

The July FOMC minutes suggested that even before taking into account the decline in risk assets, there was no consensus to raise rates in September to begin with. "Some" participants argued that conditions to raise rates "might not soon meet" and "some" participants were confident that conditions for raising rates would be met shortly. Those who were not confident were likely worried about downside risks from energy prices and strengthening USD as "some members continued to see downside risks to inflation from the possibility of further dollar appreciation and declines in commodity prices." Since then, energy prices have fallen and USD has strengthened further, both creating headwinds for the inflation outlook over the coming quarters.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Tepid moves of 10Y US treasury yields on Fed’s dovish commentary

Friday, August 28, 2015 11:21 AM UTC

Editor's Picks

- Market Data

Most Popular