BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026

JPMorgan Cuts Gold Price Forecast, Sees Bullion Reaching $4,500 by End of 2026  Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target

Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

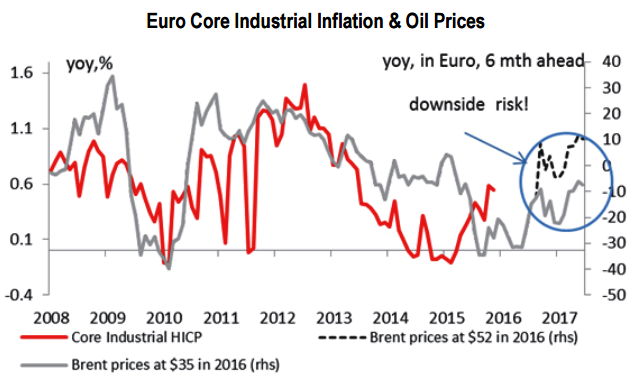

The ECB has unleashed an unprecedented series of policy measures to try and push eurozone inflation back up to levels conducive to healthy economic growth. But even the most optimistic forecasts suggest that it could well be quite some time before inflation in the euro area returns to near target levels. Rout in oil prices constitutes a significant downside risk to the ECB's inflation expectations and is likely to refuel talks of further monetary accommodation from the central bank.

In early December, the ECB cut its deposit rate by 0.1% to -0.3% and revised down its inflation forecasts for 2017 by 0.1%, both on headline and core to respectively 1.6% and 1.5%. However, the forecasts were made under the assumption that Brent prices will average $52.2 and $57.5, respectively, for 2016 and 2017. The ECB assumed favourable base effects in energy prices will likely help push up inflation by 1.3% between November 2015 and October 2016, which is unlikely to be met! With forecasts for oil at $35, base effect linked to energy prices for 2016 could be roughly half the ECB's expectations.

Also, there is a growing sensitivity between short term inflation trends and medium term inflation expectations which the ECB called the risk of "un-anchoring inflation expectations". In financial markets, this has been visible through a rising correlation between oil prices and 5Y in 5Y inflation swaps. Indeed, in recent months there has been a rising inverted correlation between 5y in 5y inflation swaps and the EUR/ USD. A weaker exchange rate is seen as the key to limit this risk.

There's not much the ECB can do to control the oil prices. Crude oil slid to its lowest levels since 2004 on Monday. There is some pass-through from lower oil prices into EZ core inflation, which would, in particular, mainly impact core industrial goods in the months ahead. So, the lower the oil price, the lower the EUR/USD needs to be! This adds to pressure on the ECB to further "recalibrate" its monetary policy in 2016.

"While Eurozone inflation would still pick up in the coming two months, it will only reach a high point at around 0.6% y/y in January. Beyond this, inflation would once again move down before reaccelerating only in H2. So, all in all, Eurozone y/y inflation next year could be more around 0.5%/0.6% vs. 1.0% expected by the ECB and with a high risk in the first half of the year to see it once again cruising around the 0.0% y/y line", says Scotiabank in a research note.

Oil prices rose around one percent on Tuesday, bouncing off Monday's 11-year lows as investors closed bearish positions ahead of the year-end holiday but the global oversupply picture capped gains. EUR/USD was trading at 1.0927 as of 1115 GMT, while Brent futures traded up 29 cents $36.64 a barrel at 0917 GMT, recovering from an 11-year low of $36.04 hit on Monday.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Lower oil prices may add pressure on ECB to “recalibrate” monetary policy in 2016

Tuesday, December 22, 2015 11:42 AM UTC

Editor's Picks

- Market Data

Most Popular