US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

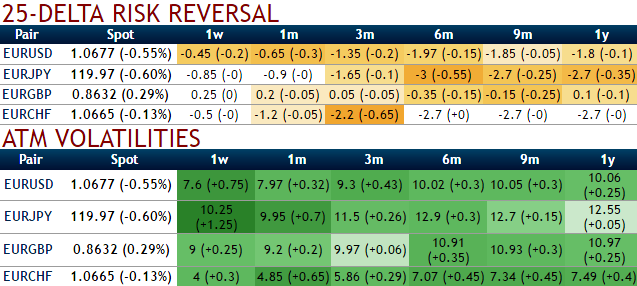

Although EUR vols appear to be at opportune levels for a fresh stab as European political hedge.

Owning protection against European political discontent has been a key pillar of our bullish vol stance since late last year but the bullishness on EUR-vol does not extend to EUR risk-reversals however. You could very well observe this in nutshell showing risk reversals for euro crosses.

Unless one can make the case for an unprecedented QE-like monetary policy innovation that spurs a 20% decline in the Euro, it is difficult to see EUR skews buck their long-run track record of underperformance (see above chart).

That kind of dramatic spot move is not in our baseline forecast: we project only a shallow dip in EURUSD towards 1.04 in H1, which implies that directional bettors on Euro weakness are better-off reprising the usual suite of put spreads or digital option structures.

The latter are well-priced in particular after the creep higher in spot this year: 4M 1.00 strike EUR put/USD call digitals that covers the French Presidential vote (a potential source of shock) but not the parliamentary elections (harder for the National Front to carry, hence a potential restorer of sanity) costs 10% of EUR notional on mids, which is excellent leverage for a barely 1-sigma spot move over the life of the trade.