Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher

Gold Pulls Back After Hitting $4,180 as Geopolitical Risk Sends Crude Higher  Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook

Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook  Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027

Goldman Sachs Raises USD/JPY Forecast, Sees Yen Weakness Persist Through 2027  Trump has made more than $1 billion from crypto in a year. How?

Trump has made more than $1 billion from crypto in a year. How?  Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks

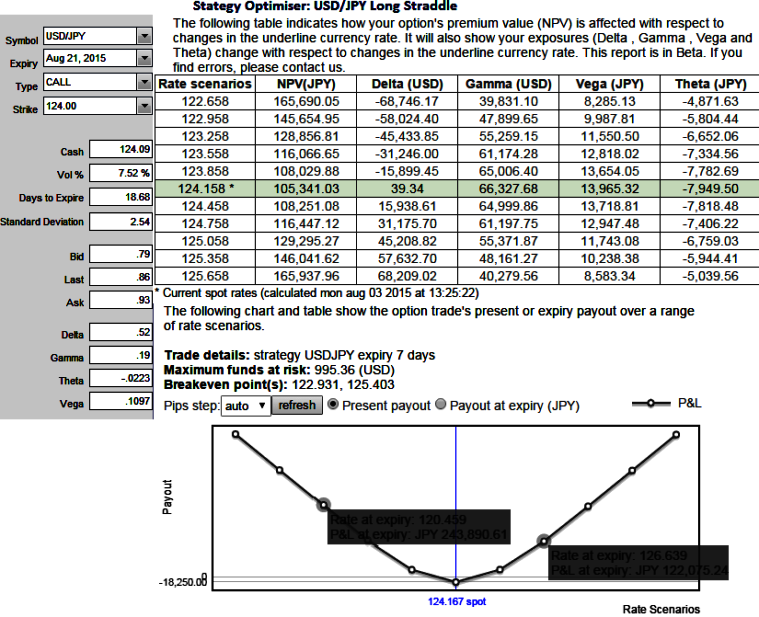

This recommendation must be quite baffling for the one who referred our earlier write up on USD/JPY on speculation grounds. If on a short straddle combination where a call and put options are written with delta's of 0.50 and -0.49 respectively how can this execution be delta hedged? The position is 1 of each written (underlying exchange price at 124.060 and ATM strike price at 124.050 with 7 days maturity).

As you can this from above charts the computation of the delta of the long straddle position is almost neutralized (closer to zero) and then a position in the underlying currency with -1*delta of the derivative position. Then have arrangements for adjusting the hedge so that it moves with the delta of the derivative position.

There is a reason for doing this, as the pair is perceived to be in range bounded and those who've taken this long straddle position can go for this arrangement by taking outright positions in spot Fx market but the person who has to ask how to do it doesn't know that reason. Write a straddle and you are short gamma and vega. You were delta hedging a position that is all about gamma and vega, all our bells and whistles would go off.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: USD/JPY delta hedging of long straddles for long term foreign traders

Monday, August 3, 2015 8:22 AM UTC

Editor's Picks

- Market Data

Most Popular