Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

Gold's 365-Day EMA Streak Since Oct 2023 Faces Its First Real Test at $3,980 — Break or Bounce to $4,140?

First, the direction of GBP de-leveraging (pound strength) is against the grain of risk-reversals i.e. in the direction of lower, not higher vol on the skew. There is a case to be made then that unlike short expiries that respond to immediate spot developments, longer-tenor (6M –1Y) vols should remain much better behaved and probably even head lower once the dust settles.

History strongly argues in favor of such muted vega response: The above table shows that 5%-10% quarterly spot moves in GBP keep 1Y ATMs more or less unchanged on average, with a sharp skew towards vol weakness rather than strength. Larger than 10% spot rallies almost always lead to material vol compression, but the inference could be distorted by the post-GFC experience of a V-shaped sterling rebound and inverse V-shaped vol collapse following the introduction of US QE which is not an appropriate lens to view the current episode.

Second, Abenomics may be a flawed template to use for gauging GBP vol behavior in the current instance due to the absence of structured product effects on the same scale as in yen: recall that spot-vol correlation in USDJPY had turned sharply higher (positive) during the 2012-13 period due to a flip in the dVega/dSpot profile of FX option books, as the traditional PRDC-driven inverse spot-vol link was upended by Japanese importer structures seeking to take advantage of yen weakness.

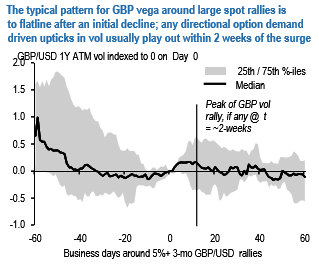

The resulting vega hedging demand as spot climbed is unlikely to be replicated in a GBP context where structured option flows are thinner. Our bias is to not stand in the way of the first flush of any GBPcall buying over the next few weeks, but to fade any eventual rally by selling 9M –1Y vol along upward sloping vol curves across the GBP complex. From a tactical timing standpoint, the pattern of 1Y ATM behavior around large GBP rallies suggests that vols do not locally top out till about 2-weeks into the spot spike (refer above chart), hence we are content to bide our time in the hope of higher back-end vols to sell in coming weeks.