Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data

If 2020 is a year in which the reflation trade becomes as dominant as in 2017, NEER depreciation could be large. The decline could be even larger than in 2017, given that in that year, the JGB 10-year yield was positive, as was the carry from investing in FX-hedged 10-year US treasuries. We also note that Japan’s trade surplus was still around 1% of GDP. By contrast, Japan’s trade surplus will be essentially flat next year. Two other factors could contribute to sustained outflows, depressing the NEER:

JGB 10-year yields were still positive in 2017 and 2018, after the BoJ introduced its yield curve control policy. However, from early 2019, yields entered negative territory, and remained negative for the most part. This episode of negative rates has already outlasted that of 2016 when yields first dipped below zero; Japanese investors are finding themselves in an unprecedented period of negative yields.

Around JPY50 trillion of JGBs held by investors other than the BoJ is set to mature in 2020, against only JPY11 trillion yen of positive yielding ultra-long-term bonds.

The global downturns have typically prompted JPY appreciation, current positioning suggests less favorable conditions for rapid JPY strength even if US recession fears re-intensify in 2020. While there is no denying the possibility of a global recession leading to relatively large Yen appreciation, we think rapid JPY appreciation is less likely even if concerns over a 2020 US recession intensify.

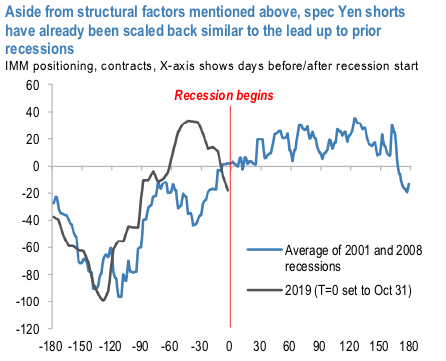

One reason for the Yen’s appreciation when entering a global recession is that investors with speculative JPY short positions face increased volatility and buy back JPY to close their short positions; we note that there was a rapid reduction in speculative Yen shorts leading into the start of the 2008-09 recession in particular, as market recession expectations were re-aligned (refer 1st exhibit).

OTC outlook: The positively skewed IVs of 3m tenors are signifying the hedging interests for the bearish risks (refer 2nd exhibit). The bids for OTM puts expect that the underlying spot FX likely to show further dips so that OTM instruments would expire in-the-money (bids up to 119.50 levels).

Most importantly, to substantiate the above indications, we could see some minor positive shifts in existing bearish risk reversal (RR) set-up of EURJPY that indicates the long-term hedging sentiments across all tenors are still substantiating bearish risks amid minor abrupt upswings in the short-term (refer 3rd exhibit). Please be noted that 3m negative RRs suggest the overall OTC hedging sentiments for the further bearish risks. Hence, we advocate below hedging strategy contemplating the current OTC indications.

Options Strategy: Contemplating above factors, we’ve advocated buying 3m EURJPY (1%) ITM -0.79 delta puts for aggressive bears on hedging as well as trading grounds as the mild abrupt upswings were contemplated earlier.

Short hedge: Alternatively, we advocated shorts in futures contracts of far-month tenors with a view to arresting potential dips, since further price dips are foreseen we would like to uphold the same strategy by rolling over these contracts for March month deliveries. Source: Sentry, JPM & Saxobank