J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead

SpaceX Stock Gets $175 Target as Analysts See Massive Growth Ahead  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns

Bank Regulation Rollbacks in the U.S. and UK Could Increase Financial Risks, Study Warns  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Futures contracts in Comex for the yellow metal has shed around $3.00, or about 0.3%, to $1,255.29 a troy ounce by 07:00GMT.

Front-end and intermediate US Treasury yields declined 1-4bp, as CPI disappointed relative to expectations, suggesting a slowing in underlying inflation.

While the weakness in CPI gives us pause, we think the FOMC is on track to raise rates again in June: the unemployment rate sits at its lowest level in more than a decade and below the Fed’s near-term and longer-run projections.

Hold 3-year duration shorts. The collapse in FRA/OIS spreads looks somewhat overdone, but the recovery could be slow and fitful. Fair value and dealer positioning support higher vols; buy the 3Mx5Y straddle.

The precious metal is sensitive to moves in U.S. rates, which lift the opportunity cost of holding non-yielding assets such as bullion. A gradual path to higher rates is seen as less of a threat to gold prices than a swift series of increases.

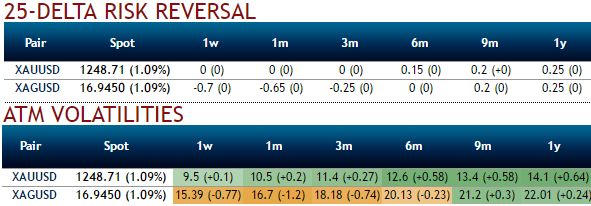

Elsewhere, OTC bullion market indicates uncertainties about bullion prices, the above sensitivity tool evidencing delta risk reversals and IV skews evidence gold prices’ momentary edginess and upside risks in long run. Positively skewed IVs of 2m tenors indicates hedgers’ interests in both OTM put and call strikes, while neutral delta risk reversal number indicates topsy-turvy swings in this precious commodity prices.

Thus, envisioning the short term range bounded trend and uncertain trend in long term from above OTC market’s rationale; we reckon that the calendar straddle would be more advantageous to keep priced fluctuations on the check.

The strategy could be executed by shorting a near-term straddle while buying a longer term straddle with an intention to profit from the rapid time decay of the near-term options sold.

Well, it is a limited return with the limited risk strategy entered by the options trader who ponders over that the underlying spot commodity price would experience very little volatility in the near term (please refer above nutshell).

Execution: Stay short in ATM call and ATM put of 1m expiry, while simultaneously buy 6m +0.51 delta call and -0.49 delta put of the similar tenor at net debit.

Maximum loss for the calendar straddle is limited and is likely incurred when the spot price had moved hugely in either direction on the expiration of the near-term straddle.