China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  How Donald Trump has changed the way diplomacy is done

How Donald Trump has changed the way diplomacy is done  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

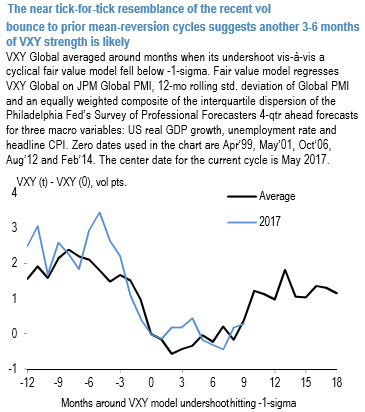

The currency market has been acting as the adjustment factor between countries positioned at different parts of the economic cycle clock. It has been one of the few assets on which carrying long volatility positions has not been a constant pain. It has also led to a dramatic reversal in the correlation regime, leading to some significant discounts on equity options contingent to currency levels.

FX vols have almost entirely retraced their peak-to-trough jump as the VIX spike of early February has subsided, but are entering March with a renewed bid under the cloud of trade tensions. Aside from the yen for which the direction of travel is clearer than elsewhere, most other USD pairs are subject to cross-currents of US twin deficits, a potentially more-hawkish-than-expected Fed, and negative trade-related headlines, hence it is unclear whether options will receive enough directional sponsorship from an unambiguous dollar trend to send implied vols spiraling higher as happened in January.

At the same time, a choppy range in the dollar should arrest the decline in realized volatility following the VIX shock, and VXY should remain in the ascendant track of its typical recovery pattern from cyclical troughs for the next 3-6 months (refer above chart). Net-net, the bar for vol selling is high in this climate, but we are not averse to selective RV constructs that take advantage of the cheapness of EUR/high-beta cross vols.

We also favor positioning for a muted dollar environment via soft short USD-correlation structures such as vanilla USD-JPY-NZD correlation triangles that net collect premium but with the hedge protection of a high-beta cross-yen leg. Given the historical precedent of de-coupling between reserve and commodity/carry currencies during trade conflicts, owning select EUR-and JPY cross vols that benefit from such a wedge is perhaps the cleanest theme at present; we are already positioned for this through GBPJPY – USDJPY and BRLJPY – USDJPY vega spreads, and add a soft, net premium-earning version of the same through a correlation triplet. Courtesy: JPM

FxWirePro launches Absolute Return Managed Program. For more details, visit: