China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

FX markets found a footing this week despite a shaky start. Following Trump’s announcement last week of 10% tariffs on the remaining $300bn of imports from China, trade tensions appeared to have escalated even further. China ordered a suspension of US agriculture purchases and the CNY fix on Monday indicated a bias for a weaker currency which shook markets and prompted the US to give China the designation a currency manipulator.

As trade tensions simmer, central banks have responded in a race to the bottom, as several of them cut rates pre-emptively given rising global risks. In G10, the prime example of this was the RBNZ who delivered a surprise 50bp rate cut (25bp was expected). In EM, India, Thailand, and Philippines all cut rates this week as well. The net result was that rates fell even more across the board. Within G10, the outperformance came mostly from currencies where the central banks have limited room to cut rates — EUR, SEK, CHF and JPY all outperformed.

The currencies with safe-haven sentiments only price in the growth revisions in hand thus far:

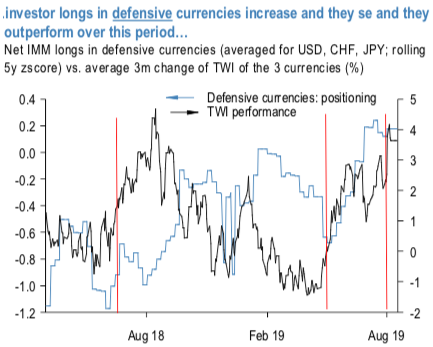

At this time, a perspective of defensive currencies appear fairly priced to only the growth outlook revisions that have occurred thus far and that additional growth vulnerabilities are not yet discounted (refer 3rd chart). The timelier indicators of growth momentum are still negative for nearly 2/3rdof the countries we cover so still indicating downside risks to growth.

In addition, investor positioning does not appear to be that crowded yet (refer 4th chart). Investor positioning becomes more defensive in the subsequent months as well in JPY, USD and CHF longs typically increase (1st chart; blue line) while investor positioning in high beta FX tends to decline (refer 2nd chart; grey line); and staying short in antipodeans (AUD, NZD) and EUR; longs in safe-havens JPY, CHF.

The backdrop leaves us defensive on FX, although admittedly the combination of poor liquidity in August and headline risk will likely keep market moves erratic. We remain positioned along with the three themes of:

1) Short high beta FX where central banks are likely to keep easing and have the room to ease further (AUD, NZD),

2) long a combination of JPY, CHF, and JPY on trade tensions, soft global growth, and late-cycle dynamics, and

3) Short EUR vs CHF and JPY on ECB easing and poor growth (recent Italian political developments are unlikely to have a sustained impact on EUR; more on this below).

While you observe AUD’s underperformance in the medium-term perspective since August 2018, was majorly due to the cooler outlook for global growth, with China especially in focus, as well as growing expectations of RBA rate cuts. AUDNZD is extremely undervalued, according to interest rates and commodity prices, and there are early signs of a reversion towards fair value which could take the cross towards 1.0750 over the next few weeks. Courtesy: JPM