S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

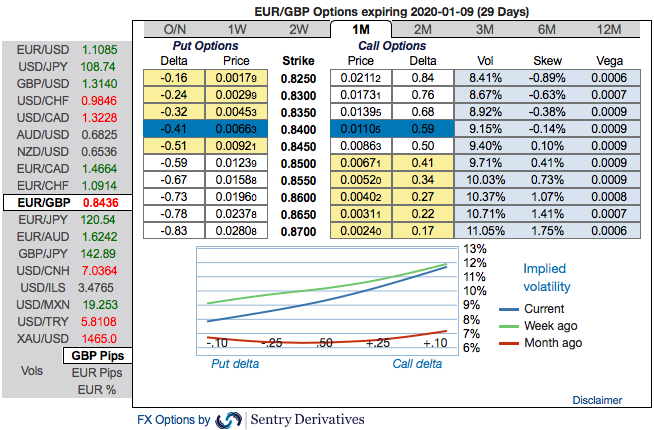

Markets remain in their current ranges as we await the FOMC and ECB meetings, the UK election and news of whether we will get a ‘phase 1’ trade deal. Data would have to be significantly away from consensus to drive the market away from the current pricing of central bank expectations and override events.

According to a highly anticipated YouGov survey, which is taking into account smaller parties, the Tories' lead is more narrow than thought so far. YouGov have said they will publish an update of their MRP (‘multilevel regression and post-stratification’) poll at 10pm tonight (its previous poll on 27 November was closely watched and predicted a 68-seat Conservative majority).

While the Labour Party is still lagging well behind the Conservative Party under Boris Johnson, the poll results suggest that the Tories might only win a slim majority. If they should even miss a majority in the end, this would be a particularly hard blow for sterling bulls.

Because not only would the pound then need to give up all its gains of the past weeks, but also the Brexit suffering of recent years would continue indefinitely, that is: There would still be no majority for a Brexit solution in Parliament, which would either lead to a "rolling EU membership" and continuing Brexit uncertainty, or in a "political accident" at some point and a hard Brexit. Certainly, all hope is not yet lost. Nevertheless, the rise in short-dated EURGBP risk reversals number seems well justified against this background.

Just before the UK’s parliamentary elections and ECB monetary policy, both scheduled for tomorrow, it's getting interesting after all.

This double-header of favourable political developments (the UK election sentiments in addition to a Brexit deal) in the near future could herald a tactical turn for the better in the general risk climate.

Hence, our defensive stance in EURGBP has been dictated by the receding global economic tide, but we cannot ignore that political risk has been an instrumental factor in these worse macro outturns. This warrants a tactical reduction in our defensive exposure but we uphold our hedging portfolios via 3-way straddles.

The passively skewed IVs of 1m tenors are stretched are indicating upside risks, more bids are observed for OTM call strikes up to 0.87 level for 1m skews and 0.90 for 6m skews.

While EURGBP risk reversals of the existing bullish setup remain intact with fresh bids for bullish risks. Below options strategy could be deployed amid the expected turbulent conditions. According to the OTC FX surface, 3-way options straddle versus ITM puts seem to be the most suitable strategy for EURGBP contemplating some OTC sentiments and geopolitical aspects.

Options Strategy: The strategy comprises of at the money +0.51 delta call and at the money -0.49 delta put options of 2m tenors, simultaneously, short (1%) ITM put of 2w tenors. The strategy could be executed at net debit but with a reduced trading cost.

Hence, on hedging as well as trading grounds, initiate above positions with a view of arresting potential FX risks on either side but slightly favoring short-term bearish risks. Courtesy: Sentrix, Saxo & Commerzbank