Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

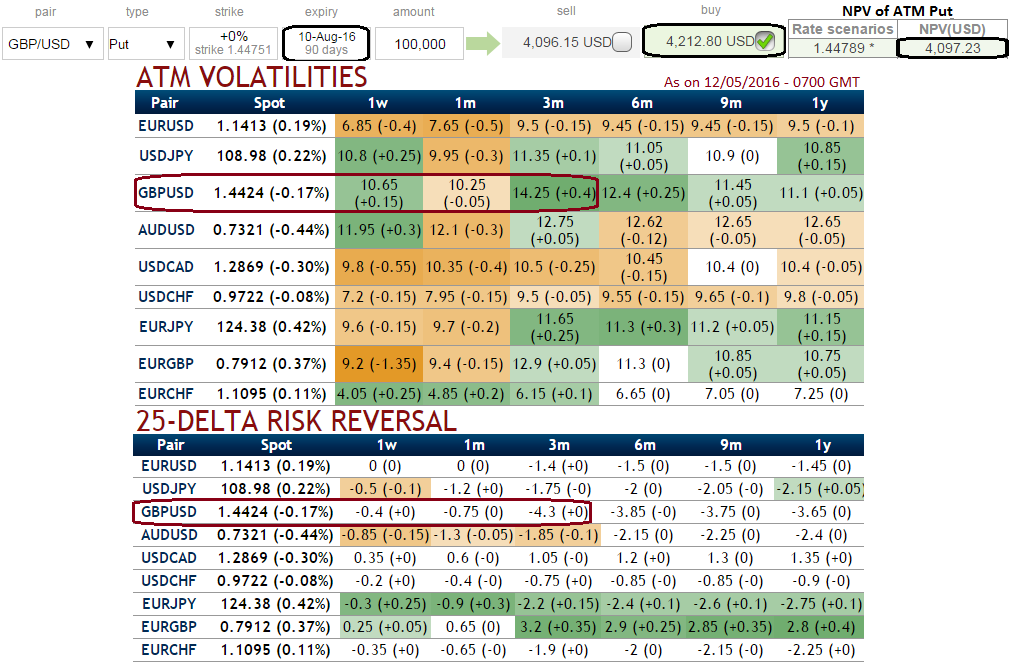

Here in this article, the primary emphasis would be on 3 months OTC arrangements:

GBP/USD gains major share in OTC markets in next 3 months’ tenors.

3M IV is trading at 14.25% which is highest among G10 currency segment, (earlier 15.23%) which is highest level in last 70 months, IV touched 16.9% in May 2010, when Prime Minister Cameron was suffering coalition issues post-election.

With the adjustment to the IVs, risk reversals and next significant event that can have the major impact on GBPUSD would be UK referendum (that is scheduled on 23rd June, approximately one and half months from now).

Pound just snapped back from critical lows against Dollar so far in last 3 months or so but price actions clearly suggests vulnerabilities still linger. Over the past 2 weeks, Pound has dropped more than 400 pips against Dollar but recovered a bit.

We would still recommend a GBP/USD 3M risk reversal i/o 1Y as a generic hedge for Brexit risk. The ideal entry point is not ideal given the near doubling of the risk reversal since early October, but the bias is for further widening of the skew in 1H on slow-bleed demand for event protection.

As the risk reversals for 1W-1M expiries also indicate that the puts have been relatively expensive and as stated above traders are willing to pay higher implied volatility prices as the strike price grows aggressively out of the money. Demand for GBP puts/USD calls have spiked on fears of UK exit from the EU.

To substantiate, we would foresee GBP on weaker side on BoE's alerts of the economic risks if Britain votes to leave the European Union, saying on Thursday that sterling could tumble harshly and unemployment would probably rise. The central bank sends this caution of this event risk after leaving their bank rates unchanged at 0.50%.

Hedging bets:

While delta risk reversals are still flashing up progressively with positive numbers that favours bulls and indicates they are willing to pay OTM strikes in higher vols.

But if have a look at the ATM put options, they seem to be available in cheaper prices while comparing with Net Present Values.

ATM puts of 3M tenors are trading just 2.8% more than net present value whereas 3M IVs are flashing above 14.25%.