Vietnam’s population hit the 100 million milestone. Where’s it headed?

Vietnam’s population hit the 100 million milestone. Where’s it headed?  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails

Gold Surges Past $4150 on Dovish Fed Signals and Weak Jobs Data; Bullish Outlook Prevails  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season

Goldman Sachs Flags 3 Key Risks Ahead of Europe’s Earnings Season  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook

Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook

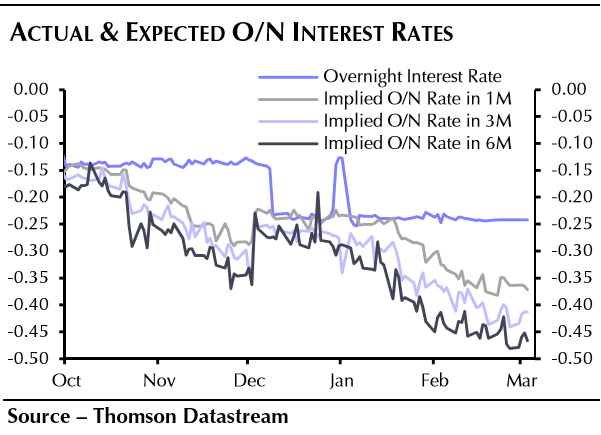

The main focus of this week is the ECB's monetary policy meeting that is scheduled on Thursday for the rate decision.

The ECB has signalled a dovish tone in its policy minutes, so additional loosening of monetary policy at its upcoming meeting on 10th March is expected.

While December's under-deliverance highlights the risk of disappointment, the deteriorating economic outlook should persuade the Governing Council to be quite more dovish this time.

A 20 bps cut in its deposit rate and a €20bn expansion of its monthly asset purchases are expected from this policy.

Accordingly, the interest rate swap markets appear to be anticipating a fall in overnight interest rates - and, hence, the ECB's deposit rate (see implied rates) - of a bit more than 10 bps at this meeting, with another cut in later months.

But a Reuters poll of economists also revealed a strong expectation of a rise in the ECB's asset purchases from the current rate of €60bn per month.

The median forecast was a rise to €70bn but the range was from €70bn to €90bn - i.e. all 66 respondents predicted a faster pace of asset purchases.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: Euro implied rates in swaps signal ECB monetary policy's dovish hopes

Tuesday, March 8, 2016 1:26 PM UTC

Editor's Picks

- Market Data

Most Popular