Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

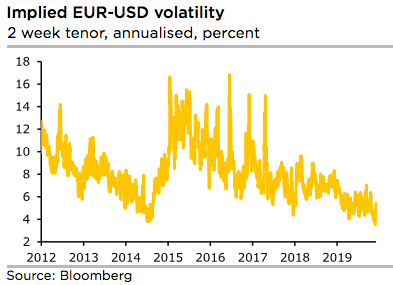

The prolonged low implied EURUSD volatility (refer above chart) indicates that the market still firmly believes that the introduction of tariffs planned for 15th December would be postponed. This optimism is no doubt admirable in view of the often rather volatile seeming nature of the US President and as the market was already caught by surprise and thus had been hit hard by Trump wielding the tariffs club in mid-2019.

Or the market underestimates the Fed and its sensitivity as regards the trade war. As in the end the reaction of the US central bank is what is decisive for USD exchange rates. Most recently the central bankers sounded much more confident which did indeed point towards a longer rate pause and thus a USD neutral monetary policy. However, that is likely to change if the trade war was to escalate again.

Admittedly in this case too a rise in volatilities back to “normal levels” would still be unlikely as the Fed’s scope to lower interest rates is pretty limited these days as well. The structurally low volatility environment is thus likely to persist in view of the limited potential for rate changes.

Moreover, today’s economic data are unlikely to ignite too much passion. Instead, markets will remain focused on the UK election which is now just a week away and, less parochially, prospects for a US-China ‘skinny’ trade deal. Market sentiment has to-and- froed after President Trump on Tuesday appeared to suggest that a deal may not be forthcoming, only for indications of a deal to resurface yesterday.

Eurostat today is expected to confirm Q3 GDP growth of 0.2%q/q in the Eurozone – not a great outturn, but not terrible either. It would in fact be slightly stronger than the ECB predicted. Moreover, some recent surveys have pointed to signs of stabilisation in business confidence.

3M EURUSD IVs would hardly be stuck around the 4-5% mark. If one ignores GBP volatility though the FX market has returned to the vol lows seen last summer. The hopes are lingering that the vol levels seen at the time would be short-lived was correct in the sense that volatilities rose significantly in August.

However, there is no sustainable escape from the structural low volatility environment - that much has become clear. That is seemingly positive for all those for whom FX is an undesirable risk.

IV factor is highly imperative in FX option dynamics because the option pricing significantly depends on future volatility, and it is quite impossible for any veteran to ascertain accurate future volatility.

Contemplating low IV environment, on trading grounds, we recommend executing butterfly spread.

So, buy 1m EURUSD OTM -0.49 delta put while simultaneously shorting ATM put of similar expiries and 1m buy OTM 0.51 delta call while simultaneously shorting an ATM call with similar expiries. This strategy is structured for a larger probability of earning a smaller but certain profit as EURUSD is perceived to have a low volatility.

Alternatively, we advocate longs in EURUSD futures contracts of December’19 delivery, simultaneously, shorts in futures of Feruary’20 delivery for the major downtrend. The short leg is likely to hedge potential slumps and the momentary upside risks can be arrested by the long leg. Thereby, one could be able to directionally position in their FX exposures on hedging grounds. Courtesy: Saxo & Commerzbank