US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Fed Confirms Rate Meeting Schedule Despite Severe Winter Storm in Washington D.C.

Fed Confirms Rate Meeting Schedule Despite Severe Winter Storm in Washington D.C.  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  RBA Raises Interest Rates by 25 Basis Points as Inflation Pressures Persist

RBA Raises Interest Rates by 25 Basis Points as Inflation Pressures Persist  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?

BTC Flat at $89,300 Despite $1.02B ETF Exodus — Buy the Dip Toward $107K?  Bank of England Expected to Hold Interest Rates at 3.75% as Inflation Remains Elevated

Bank of England Expected to Hold Interest Rates at 3.75% as Inflation Remains Elevated  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings

Nasdaq Proposes Fast-Track Rule to Accelerate Index Inclusion for Major New Listings

Australian central bank (RBA) is scheduled for its monetary policy next week wherein it announces cash rates. With the RBA expected to be on hold for the foreseeable future short-maturity interest rates are well anchored. While 3y swap rates have been in a 2.10 – 2.35% range throughout 2018.

The Aussie’s mid-August slide to 0.72 on Turkey-inspired global risk aversion left it quite oversold when judged by our short-term fair value estimate, which remains near 0.75. AU-US yield differentials have continued to drift in the US dollar’s favour in recent weeks but Australia’s key commodity prices have been mixed, overall a little higher since mid-August and a long way above March lows. Still, AUD risks probably remain to the downside in September (0.70 handle), given the confluence of FOMC meeting, US review of China tariffs and EUR/Italy budget risks. By year-end we see AUDUSD back to 0.73.

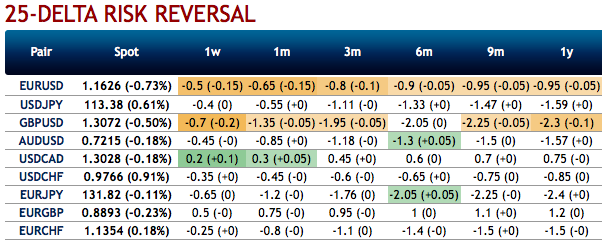

AUDUSD risk-reversals (RRs): AUDUSD RRs have been bullish neutral (refer above nutshell). It is disingenuous to include AUD in an EM list, but its China / commodity linkages have resulted in a price response this year not too dissimilar from other EMs, hence this (questionable) stretch.

With spec AUD positions fairly short on IMMs, there is room for a short squeeze higher in the currency that can dampen the elevated negative spot-vol correlation of recent weeks.

Thus, we intend shorting 3M 25D AUD puts vs 6M 25D AUD calls, vega-neutral in a box risk-reversal structure. This construct is net short gamma and skew, and can be construed as a moderately RV efficient way of selling AUD vol (refer 2nddiagram).

Currency Strength Index: FxWirePro's hourly AUD is flashing -26 (mildly bearish), hourly USD spot index is inching towards 84 levels (which is bullish), while articulating at (12:19 GMT). Courtesy: JPM

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex