China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says

China’s AI Manufacturing Boom Masks Weak Consumer Economy, Citi Says  J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600

Sell the Bounce": Gold Rally Stalls Near $4165 as Fed Hawks Slam the Door on Rate Cuts — Targets $4000/$3600  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch

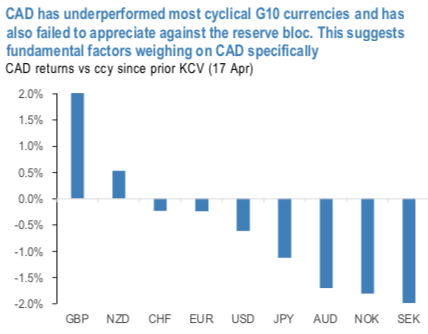

In the G10 space, CAD has lagged both cyclical and reserve currencies (refer 1st chart). That CAD has not even outperformed the reserve bloc is indicative that CAD is not simply underperforming because of its inherently lower beta amid the recent modest relief rally, and is instead being dragged down by a mix of idiosyncratic fundamental factors, which we discuss below. This behavior further solidifies our conviction that on a broad-basis, CAD will be one of the distinct underperformers in G10 FX this year.

Bearish CADJPY Scenarios:

1) The global sudden stop catalyzes a large capital outflow given Canada’s BoP deficits or

2) The renewed oil price war accelerates industry-wide crude production shut-ins.

3) COVID-19 fears re-intensify significantly, leading to multiple waves of infections or Japan-specific rises in case numbers;

4) Assessments for the prospect of a V- shaped global growth recovery are significantly tested;

5) Trade tensions between the US and China re-intensify with negative spill-overs to Japan’s supply chain.

Bullish CADJPY Scenarios:

1) The COVID-19 downturn is a true v-shaped recovery.

2) The outlook for the global economy recovers more sharply than expected and risk sentiment firms;

3) Momentum in JPY selling flows related to outward portfolio investments and FDI repeats on a similar exceptionally large scale as seen in 1Q’20.

Despite this recent beta-driven CAD strength, the view for underperformance in 2020 on domestic factor still holds amid pandemic Covid-19, though may be less front-loaded than originally expected. This view has been predicated on an expected dovish BoC responding to a broadly-weaker economy, potentially forced to ‘catch up’ to other central banks globally, having earlier eschewed rate cuts in 2019, thereby warranting some catch-up CAD weakness.

OTC Updates and Options Strategy:

The positively skewed CADJPY IVs of 6m tenors have still been signaling bearish risks, the hedgers’ interests to bids for OTM put strikes up to 72 levels indicating downside risks in the medium terms (refer 2ndexhibit).

Accordingly, we advocated diagonal options strips strategy to address any abrupt upswings in short-run and the major downtrend.

At spot reference: 76.300 level, buying 2 lots of 3m at the money delta put option and simultaneously, buy at the money delta call options of 1m tenor. It involves buying a number of ATM call and double the number of puts. The option strip is more of customized version of options combination and more bearish version of the common straddle.

Any hedger or trader who believes the underlying currency is more likely to spike upwards in short run but major downtrend can go for this strategy. Cost of hedging would be Net Premium Paid + brokerage/commission paid. Courtesy: Sentry & JPM