J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand

J.P. Morgan Sees Potential Vestas Guidance Upgrade Amid Strong Wind Energy Demand  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies

Silver Cracks Key 365-Day EMA for First Time Since Feb 2024; Bears Eye $50 on Rallies  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill

The news that the EU was going to offer its British partners a further reaching (“super- charged”) free trade agreement than ever entered with anyone else before provided decent support for Sterling at the end of last week. The reaction was not justified for several reasons.

First of all, a free trade agreement seemed the only logical answer in view of the many “red lines” on both sides. At least the EU had made this clear often enough. It may be seen as positive that the agreement is aimed at facilitating closer relations than with other trade partners, but the extended elements refer mainly to cooperation in the area of defence, a move that is no doubt welcome but of little real economic relevance.

Secondly, the EU would therefore reject Theresa May’s Chequers Plan, according to which the UK would have de facto remained in the customs union in terms of goods trade, and would instead strengthen her rival Boris Johnson’s proposal of a Canada-plus free trade agreement; which means that May’s position would be weakened.

And thirdly, this seems to be the most important aspect in my view – the proposal still does not solve the issue of the Irish border. This week the British government wants to put forward a new proposal that will reduce the checks between Northern Ireland and the rest of Great Britain to a minimum.

Accordingly, the investigation of sterling volatilities is reprised as carried out in an earlier piece. The value of owing optionality for hedging Brexit risk is confirmed.

We consider a worst-of puts structure for hedging a scenario where wider BTP-Bund spreads could push 14% EUR lower vs G7 safe havens.

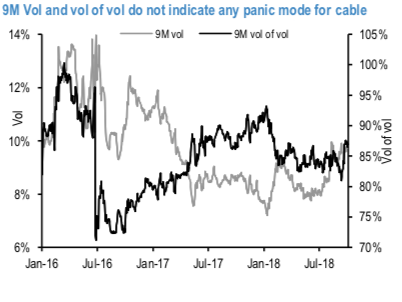

Assessing what the market is currently pricing for different scenarios, corresponding to probabilities (estimated in-house) of 60% for the EU-UK deal case vs. 20% each for no-deal and no-Brexit cases. With 9M cable- implied vol currently at 9.8% (refer above chart), we estimate the vol for the baseline scenario at 8.5% and that for the two risk-scenarios at 11.6% (up from the previous estimate at 11.2%). While the value of the high-vol mode is not low on a standalone basis and is higher than one month ago, a comparison with the patterns observed in 2016 around the Brexit referendum confirms the value of owning optionality for hedging non-core scenarios. Courtesy: JPM, Commerzbank

Currency Strength Index: FxWirePro's hourly EUR spot index is inching towards -95 levels (which is bearish), while hourly USD spot index was at 71 (bullish) while articulating (at 13:20 GMT). For more details on the index, please refer below weblink: