Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings

Bernstein Names IAG, Ryanair as Top European Airline Stocks Ahead of Earnings  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Jamie Dimon Warns Anthropic's Mythos AI Poses National Security Risks

Jamie Dimon Warns Anthropic's Mythos AI Poses National Security Risks  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Crypto Major Pair Action Bias: ETHUSD Bullish as BTCUSD, SOLUSD & XRPUSD Stay Neutral

Crypto Major Pair Action Bias: ETHUSD Bullish as BTCUSD, SOLUSD & XRPUSD Stay Neutral  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise

The currency market is in crisis mode. For EURUSD this means that usual factors such as interest rate differentials hardly count. These will only count again when the crisis is over. Then the euro could profit. While we have moved our GBP forecast path to weaker levels as a result of recent corona-related movements.

The massive spike in FX volatility in March has lifted VXY to 2-sigma rich for current macro settings, which may prove inadequate risk premium should growth conditions worsen towards 2008 extremes. A sustained cooling in realized vol is also a pre-requisite for a local peak in VXY; we are not there yet.

Severely inverted vol curves, especially in the front- end, offer an opportunity to own forward volatility as a positive carry long vol play, liquidity permitting. USDMXN and USDRUB synthetic FVA (aka gamma neutral calendars) screen as good front-end forward vol buys.

GBP vs safe haven FX correlations should fall amid GBP’s vulnerability to COVID-19 developments. We find value in defensive leveraged structures of the form (GBPUSD & USDJPY) that achieve premium savings by selling relatively high USD correlations.

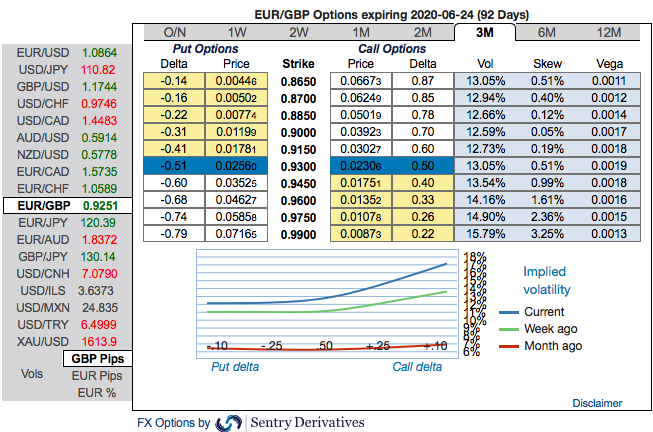

The positively skewed EURGBP IVs of 3m tenors are well-balanced, indicating both upside and downside risks, more bids are observed for OTM call strikes up to 0.99 levels.

While EURGBP risk reversals of the existing bullish setup remain intact as fresh bids for bullish risks have been added across all tenors.

According to the OTC FX surface, 3-way options straddle versus ITM puts seem to be the most suitable strategy for EURGBP amid the expected turbulent conditions contemplating some OTC sentiments and geopolitical aspects. Courtesy: JPM & Commerzbank