China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Part II — The listing: NFTs as bottle-stamps, and a vault the family is in no rush to sell

Part II — The listing: NFTs as bottle-stamps, and a vault the family is in no rush to sell  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  Economic pessimism has set in – but there are reasons for Australians to be hopeful

Economic pessimism has set in – but there are reasons for Australians to be hopeful  The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough

The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough

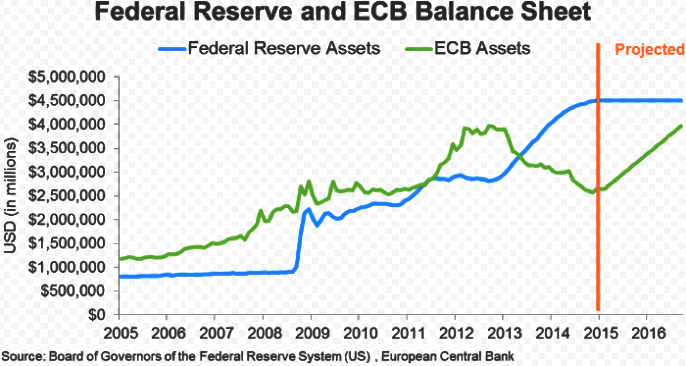

Last month of 2015, the ECB has not delivered what streets expected (not a full depo cut we had in mind i.e. -10bps versus forecasts of -20bps) but the extended QE programme we were looking for (now due to run at least until March 2017).

Slow pace of easing: The ECB has been firm for a programme of reinvestment as existing holdings mature, while many expected the expansion pace of asset purchases.

Although Draghi claims the reinvestment will add EUR 680bn to the ECB's balance sheet by 2019, it is perceived that he disappointed to a market accustomed to, (1) upfront easing and (2) Draghi over-delivering.

It is clear he had no consensus to be much more aggressive, even though promises by Draghi that further monetary stimulus could be underway, many analysts are skeptical on central bank's sizable additions to its €1.46 tn asset-purchase programme in 2016.

There were rumors of a marginal of nonconformity by eidmann/Lautenschlaeger as well as Knot/Hansson/ Rimsevics though note Weidmann and Lautenschlaeger (the two German members) are also said to have opposed the original QE announcement in Jan.

Draghi himself says "it may take years" before the EZ returns to pre-crisis unemployment rates, but "as we have seen in the UK and US, event at that point... there may still be a substantial time lag before a tight labor market translates into higher wages."

Conversely, the first Fed rate hike is finally behind us. Many were calling for a "dovish hike" but relative to already very dovish expectations, this was nothing of that sort.

FOMC members' economic projections still imply four more hikes next year, well ahead of what the market is priced for. For many, the 25% rally in DXY to its Dec peak is likely to mark the exhaustion of the trend.

However, these speculations have left the forecasts unchanged in this month (EUR/USD 1.03 end-Q1 and parity by end-Q2).

Hence, EURO could be boosted temporarily by risk aversion in its role as risk off proxy or more sustainably by signs of inflationary pressures.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

ECB’s B/S numbers despite German members’ denials to prop-up EURO while Fed’s hiking in 2016 likely to trim EUR/USD

Monday, January 4, 2016 11:41 AM UTC

Editor's Picks

- Market Data

Most Popular